20250305 - 高收入人群的退休储蓄策略 - Backdoor Roth IRA Defined & Explained The Motley Fool¶

- 分类:

Clippings - 创建:

2025-03-05 - 标签:

后门罗斯IRA, 退休储蓄, 传统IRA, 罗斯IRA, 税务规划, 投资策略, 收入限制, 转换, 贡献限额

Backdoor Roth IRA: Defined & Explained | The Motley Fool¶

摘要 (Summary)¶

本文介绍了后门罗斯IRA的策略,这是高收入人群通过传统IRA转换为罗斯IRA的一种方法。由于直接向罗斯IRA的贡献有收入限制,但转换没有限制,因此即使收入超出罗斯IRA直接贡献的限制,仍可以通过后门策略进行投资。后门罗斯IRA的步骤包括向传统IRA缴款,然后立即转换为罗斯IRA。文章还提供了2024年和2025年的罗斯IRA贡献限额,并讨论了转换时可能产生的税务影响。最后,文章建议在决定是否使用后门罗斯IRA策略时,需考虑个人税务情况和退休计划。

要点 (Key Facts)¶

- 2024年和2025年罗斯IRA的贡献限额分别为每人7,000美元或50岁及以上的人8,000美元。

- 罗斯IRA直接贡献有收入限制,但转换没有收入限制。

- 后门罗斯IRA策略涉及先向传统IRA缴款,然后转换为罗斯IRA。

- 如果传统IRA中有其他可扣税资产,转换时需要按比例计算应纳税收入。

- 后门罗斯IRA的税务影响取决于转换时是否有应纳税收入。

- 罗斯IRA无需最低分配额(RMDs),并且可以随时提取贡献金。

正文 (Content)¶

Funding a Roth IRA is the best way to take advantage of current low income tax rates and set yourself up for years of tax-free income in retirement. However, people with high incomes are not allowed to contribute to a Roth IRA directly. For them the only way into a Roth is through the back door -- with a strategy appropriately known as the backdoor Roth.

Image source: The Motley Fool

Understanding backdoor Roth IRAs¶

Here's the key point to know before we go any further. Even though there are income limits on Roth contributions, there aren't any limits on Roth conversions. You can earn as much as you want and still convert a traditional IRA to a Roth.

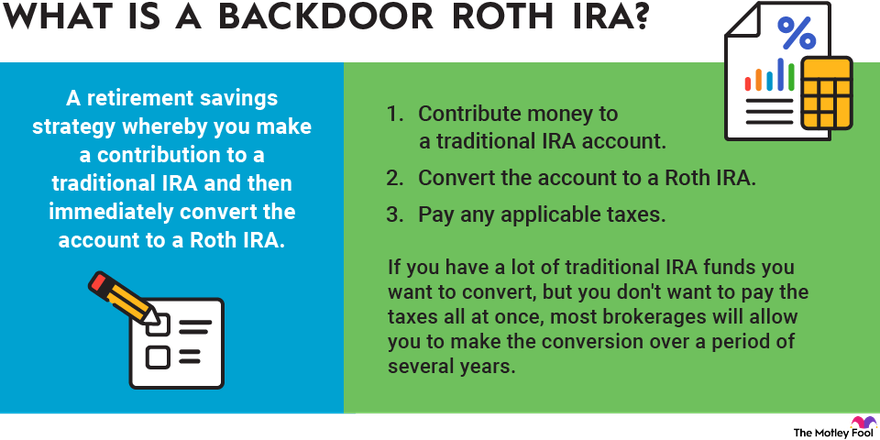

A backdoor Roth IRA is a retirement savings strategy whereby you make a contribution to a traditional IRA, which anyone is allowed to do, and then immediately convert the account to a Roth IRA.

First, let's take a step back and see if you can contribute to a Roth IRA directly.

For you to contribute directly to a Roth IRA, your income must be under a threshold dependent on your tax filing status. If your income is above a defined upper limit, also known as the phase-out limit, then you can't contribute to a Roth IRA at all. Within a range just below that upper limit, only partial Roth IRA contributions are allowed. The IRS sets these limits each year. Here's a look at the 2024 and 2025 limits:

Roth IRA contribution limits for 2024 and 2025¶

| Tax Filing Status | Maximum AGI for Full Roth Contribution | Phase-Out (Upper) Income Limit |

|---|---|---|

| Single, head of household, or married filing separately IF you didn't live with your spouse during the year | $146,000 (2024); $150,000 (2025) | $161,000 (2024); $165,000 (2025) |

| Married filing jointly or qualifying widow or widower | $230,000 (2024); $236,000 (2025) | $240,000 (2024); $246,000 (2025) |

| Married filing separately IF you lived with your spouse at any point during the year | $0 | $10,000 |

If your income is above the phase-out limit, you're out of luck for making a direct Roth contribution. But you can still make a contribution to a traditional IRA, and that's where the backdoor Roth strategy comes in.

Backdoor Roth IRA contribution limit¶

The IRA contribution limit for 2024 and 2025 is $7,000 per person, or $8,000 if the account owner is 50 or older. In 2024, the contribution limits rise to $7,000, or $8,000 for those 50 and older. So if you want to open an account and then use the backdoor IRA method to convert the account to a Roth IRA, that's the maximum you can contribute for those tax years.

It's worth noting that you can make IRA contributions until the tax deadline, so if you make your contribution after New Year's Day, you can effectively make two years' worth of contributions at once.

Are You Missing The Morning Scoop?¶

Start your day ahead of the game with the market’s top stories and key investing insights. Breakfast News delivers it all in a quick, Foolish, and free daily newsletter that lands in your inbox every market morning..

When you convert a traditional IRA to a Roth IRA, any amount that you received a traditional IRA tax deduction on will be considered taxable income.

For example, let's say that you contributed $5,000 to a traditional IRA in 2024 and claim it as a deduction on your 2024 tax return. If you then convert the account to a Roth IRA in 2024, the account value at the time of the conversion (even if it's more than $5,000) would be considered taxable income, which you would report (and pay tax on) on your 2024 tax return that's due on April 15, 2025.

On the other hand, if you make a nondeductible traditional IRA contribution or if you immediately convert the account after making a traditional IRA contribution, there generally won't be any taxes due on the conversion.

I use the word "generally" because, unfortunately, if you have additional traditional IRA assets, then there's another problem. The IRS won't let you treat the conversion as coming solely from the non-deductible IRA. Instead you'll have to include a portion of the conversion in your taxable income, based on the pro-rata value of your nondeductible and other traditional IRA assets. That's generally not desirable, so if you have extensive retirement assets in deductible traditional IRAs, you should think twice before trying to do a backdoor Roth.

How to do a backdoor Roth IRA conversion¶

The backdoor Roth IRA method is pretty easy. The general steps are:

- Contribute money to a traditional IRA account, making sure your brokerage offers Roth conversions (most do).

- Convert the account to a Roth IRA. Typically this just involves a short form, which your brokerage can provide and process.

- Pay any applicable taxes. You have until the tax deadline for the year in which the conversion was made to pay any applicable taxes on the converted account, but it's a smart idea to consider sending the money to the IRS right away.

If you have a lot of traditional IRA funds you want to convert, but you don't want to pay the taxes all at once, most brokerages will allow you to make the conversion over a period of several years.

Related retirement topics¶

Should I do a backdoor Roth IRA?¶

As you can see, the backdoor Roth strategy can be valuable in getting money into a tax-free account. And, with the possibility that tax rates go higher from here, getting money into Roth IRAs now could pay off in the long run. But it isn't right for everyone. So it's important to ask yourself (or your financial advisor) whether a Roth IRA makes sense for you or not. If you make too much to contribute to a Roth IRA directly, the answer might be no.

Think of it this way. If you are in a low tax bracket -- say 10% or 12% -- right now, it can make great financial sense to lock in your current tax rate by contributing to a Roth IRA and to not have to worry about taxes in retirement. On the other hand, if you're in a relatively high tax bracket right now and you qualify for the traditional IRA tax deduction, a traditional IRA might make more sense when it comes to tax optimization.

There's more tax certainty with a Roth IRA since there's no way to know what U.S. tax brackets will look like by the time you're ready to retire. Plus there are other benefits, such as no required minimum distributions (RMDs) and the ability to withdraw contributions whenever you want, that add value to the Roth IRA.

Just because everyone can use the backdoor method of contributing to a Roth IRA doesn't mean that everyone should. Before you start the process, make sure it's truly the best move for your retirement strategy.

Don’t miss this second chance at a potentially lucrative opportunity¶

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $300,764!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $44,730!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $524,504!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of 03/05/2025

The Motley Fool has a disclosure policy.